Talk by Prof. Enikő Vincze, housing justice activist at Căși sociale ACUM!/Social housing NOW! in Cluj, Romania, given within the seminar series organized by the Torino-based Beyond Inhabitation Lab project

A synopsis based on the recorded presentation of 21.03.2024 and the PowerPoint presentation prepared for the talk.

The talk was inspired by the results of the research project conducted between 2021 and 2023, “Class formation and re-urbanization through real estate development in a semi-peripheral country of global capitalism” (www.redurb.ro). The project’s major accomplishment is the collective volume Uneven Real Estate Development in Romania at the Intersection of Deindustrialization and Financialization, edited by Enikő Vincze, Ioana Florea, and Manuel Aalbers, forthcoming at Routledge.

The project’s emphasis on transforming industrial platforms into real estate development sites underscores the global interest in Romania’s real estate sector. The author’s interview with the CEO of Blitz Agency in April 2022 illuminated the appeal of former industrial platforms for real estate development. These sites, often in semi-central urban areas, provide the necessary infrastructure and space for large-scale redevelopment. They have the potential to optimize the price per square meter, a crucial objective for investors. Furthermore, they facilitate the creation of mixed-use real estate, aligning with the evolving urbanistic plans that no longer endorse industrial production in cities.

“Why invest in Romania?”

This is a question equally crucial for the Romanian state and the investors. The country’s favorable fiscal regime has attracted diverse investors, as evidenced by the CBRE (real estate services company) data. In the first half of 2021, the total volume of real estate investments in Romania reached 303.6 million euros, with the most significant contributions coming from Austrians, Americans, and Czechs. Buyers from South Africa, Sweden, Switzerland, Germany, and Greece also participated, while Romanians contributed only 1% to the volume of real estate investments.

The REDURB research project: fieldwork and approach

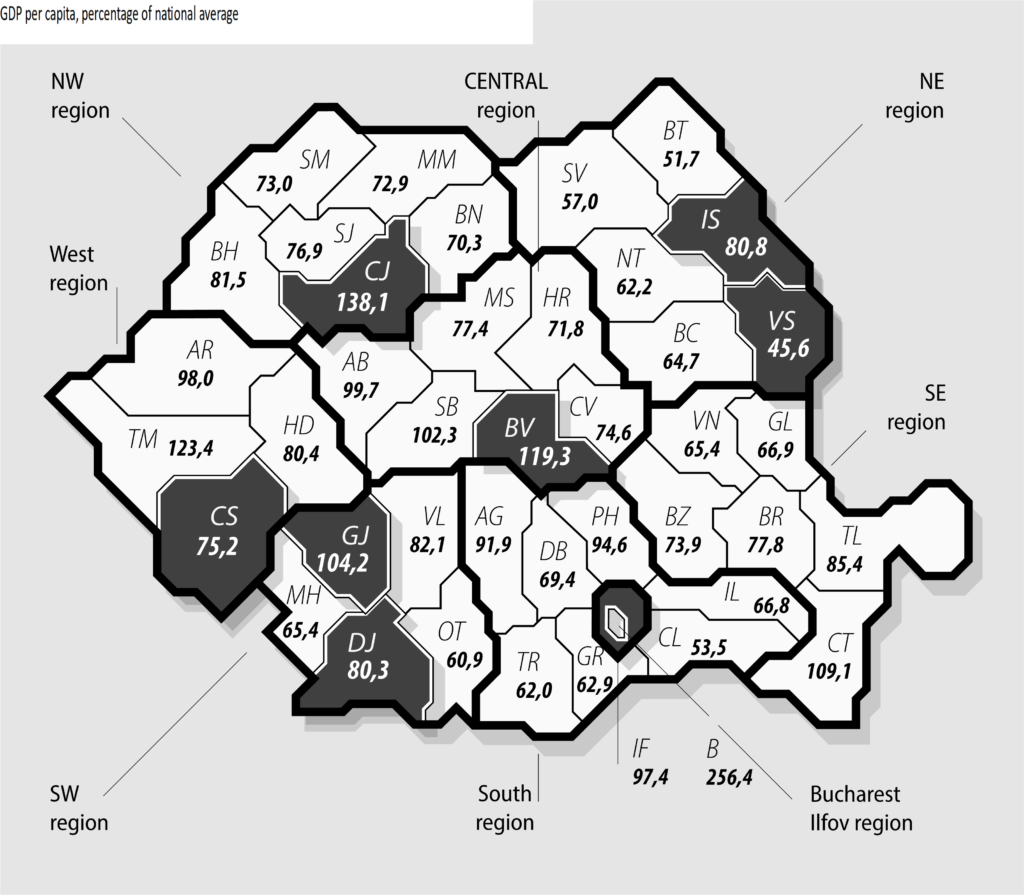

Figure 1. Romania’s counties’ GDP per capita compared to the national average GDP/capita

The REDURB research team covered four second-tier and four third-tier cities in Romania’s eight counties belonging to different development regions (see Figure 1 above): Ioana Florea (Bârlad and Iași), Sorin Gog (Reșița), Marina Mironica (Cluj), Livia Pancu (Bârlad and Iași), Mihail Sandu-Dumitriu (Bragadiru), Enikő Vincze (Cluj and Brașov), Ioana Vlad (Craiova), George Iulian Zamfir (Tg. Jiu). Figure 1 reflects the uneven development between these counties from the point of view of the percentage of GDP per capita compared to the national average.

Each team member made several field visits, collected and analyzed interviews, documents (of the World Bank/ International Monetary Fund/ European Commission, and local/national/ transnational developers/investors), databases and reports (of National Statistical Institute, Cadaster Agency, National Trade Registry Office, Romanian Central Bank, Eurostat, termene.ro, datagov.ro, CBRE, ERSTE, Property Forum, Colliers, Imobiliare.ro). Another team member, Manuel Aalbers, contributed to situating the Romanian case on the larger map of Central and Eastern Europe and the world. In his chapter prepared for our collective volume, he noted: “The ‘lumpengeography’ of deindustrialized land in Romania became a reserve space to be redeveloped, a golden opportunity for global pension fund capitalism” (forthcoming REDURB collective volume).

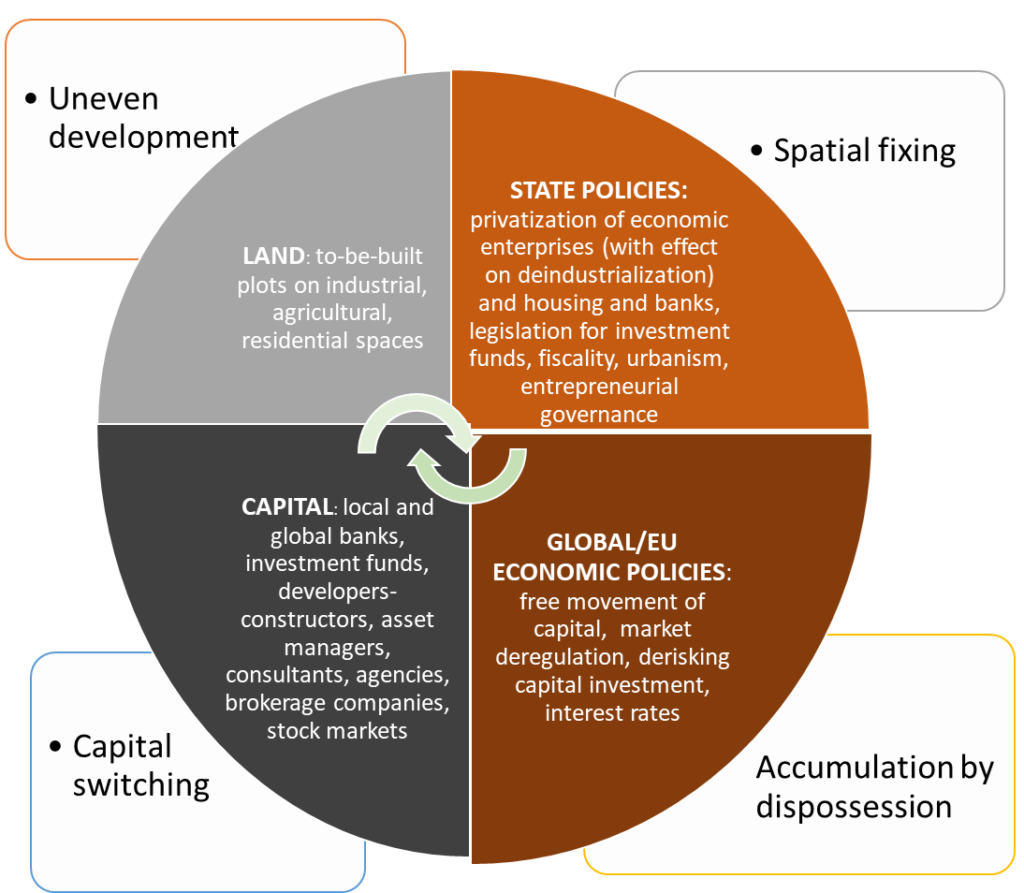

The theoretical/conceptual frame of the REDURB analysis was built on the conviction that we need to consider both global and local processes and actors and the role of both economy and politics in explaining why real estate development as a business emerged and advanced in Romania as it did. Figure 2 details the four factors revealed as necessary for the emergence and advancement of real estate development. It also shows the concepts extracted from Marxist political economy, critical geography, and urban sociology: spatial fixing and capital switching (both reflecting ways how capital solved its overaccumulation crisis since the 1970s by expanding across territories and economic sectors and circuits of capital), respectively uneven development and accumulation by dispossession (pinpointing on how peripheralization at different scales, in the relation between countries but as well as within one country between regions and cities, always creates capital accumulation opportunities).

Figure 2. The approach and conceptual scheme of the REDURB research project

The Brașov case study

The REDURB research project’s contribution to the critical study of real estate development evolves at the intersection of case studies and theorizing. The Brașov case study illustrates how private investment strategies and state interventions transformed a socialist industrial platform (Tractorul Factory) into a site for capitalist real estate development (a mixed-use Coresi district including shopping, residential, office, and hotel areas). Figure 3 reflects this change, evident in the built environment, through an old factory picture and the collage of the author’s photos taken in Brașov in 2021 and 2022.

Tractorul factory (120 hectares; 20,000 employees)

▼

Figure 3. The transformation of an industrial platform into a site of mixed-use development

The above case shows that advancing such an extensive real estate development requires an investment of 350 million euros. The investor’s expected revenues from commercial rental of 5 million euros/year and a gross rate of return via residential rental of 5% per year talk about the financialized nature of such a project. Otherwise, the global actor that ensured the possibility of this development (the real estate branch of the French multinational retail Auchan), a non-financial company in itself, is also financialized. In 2018, Auchan Holding transformed Immochan into Ceetrus to act as a global investor-developer with mixed-use projects, and even before that, in 2006, it owned 49.9% of the capital of Oney Bank. Moreover, in 2019, Ceetrus issued its first corporate Green Bonds, placing it with institutional investors for 300 million euros to (re)finance green assets (buildings) and registering them on the Luxembourg Stock Exchange.

Meanwhile, Ceetrus promotes itself on its website as “an impact property investor aiming to transform its sites sustainably for the prosperity of local communities” and calls us to “imagine a brand new world, in which cultivating life has value and caring for the fragile makes us stronger.” Nevertheless, what makes Ceetrus stronger are definitely its 8 billion euros of real estate assets, 50 development projects in 10 countries from Europe and Asia so, owning a diversified global portfolio, the 300 retail-driven sites, which were developed for rental purposes, and 20 million square meter lands that might be anytime used as a collateral for loans. In Romania, Immochan/Ceetrus owns 120 hectares of land of the former Tractorul factory and owns/ administers the Coresi Shopping Resort; additionally, in 2019, it purchased in Reșița the Mociur platform of the former Machine Building Plant, where it elaborated a master plan for a future complex development.

Regarding the local processes that made the emergence of this real estate development project on the former Tractorul from Brașov possible, one should mention, most importantly, the privatization of the factory. In 1997, Tractorul was included in the First Private Sector Adjustment Loan that Romania received with conditions from the International Bank for Reconstruction and Development. After four unsuccessful privatization attempts, in 2007, the national privatization agency decided to liquidate Tractorul through the Transylvania Insolvency Office, and measures were taken to dismiss the employees. The factory’s assets were sold to a British investment company at a competitive open auction via the local firm Flavus Investiții. The latter declared from the beginning that it wanted to use the land for real estate development, while the state pretended not to agree with this. The European Commission analyzed whether the auction was legally conducted and eventually gave a green light to it. Flavus Investiții obtained authorization for its Zonal Urbanistic Plan (ZUP), which aims to regenerate the area. Due to the crisis, the company did not start any demolition or development there. In 2012, it sold the land, buildings, and ZUP to Immochan presented above. In 2014, most of the buildings were demolished, and the first stage of the development of Coresi District as a multifunctional area began with Coresi Shopping Resort opened in 2015.

To further develop the land for a mixed-use project, Ceetrus collaborated with local developers. The most important one, Kasper Development, assumed the realization of the Coresi Avantgarden Residential Complex, completing its first stage in 2017 with more than 2000 flats, followed by a plan of making another 3000. In the interview given in October 2021, the CEO of Kasper Development presented her project and business in the following way: “I engaged in a partnership with Ceetrus in 2016 for residential development through a joint firm called Imologia. I would have never been able to accomplish such an endeavor on my own, primarily because I lacked the money to purchase 100 hectares of land. No local builder could have afforded what Immochan did. They had the money, owned the land, and were experts in such investments. We are different from other developers who earn profits from densification. … We operate with a profit margin of less than 15%, whereas most businesses in the city seek profits of at least 30%. Coresi’s business model entails planning, construction, monitoring, advertising, and sales enterprises; only a portion of the construction work is subcontracted. Currently, the typology of our customers is divided into three categories. About 65% of customers are those who buy for their use. The remaining 35% are two categories of investors, those purchasing 2-6 flats, and the more affluents buying between 10-30 flats as an investment.” In the case of the Coresi Business Campus, the collaboration between the global and a local actor was that the latter, Ascenta Management, the initial owner of 20 hectares of the old Tractorul platform, sold these parcels to Immochan in 2017, who transformed most of the old industrial halls into new office buildings, some of them keeping architectural elements of the past. Moreover, Hotel Qsmo, constructed and opened by Ceetrus in 2021, was given to the management of Kronwell, owner of a highly branded local hotel.

Additionally, the Brașov City Hall also contributed to the fulfillment of the Coresi project on a former industrial platform: it ensured the authorization of the general and zonal urbanistic plans and the demolition and construction projects; it made a street crossing the district as an infrastructure that contributed to the increase of its exchange value, it committed itself to entrepreneurial urban governance as any other city which looks to increase its local budget by attracting investors, and recently, it announced its greening plans welcomed by Ceetru’s CEO as an essential step towards making Brașov more touristic, i.e., bring more customers for its developments.

Patterns of real estate development

Real estate development on former industrial lands via urban regeneration is among the major spatial patterns of this business’s advancement. Urban sprawling (toward city peripheries and metropolitan areas, often using agricultural land or even green areas) and densification within existing districts are also major spatial patterns.

The geographical locations/ lands and buildings resulting from deindustrialization (linked to the privatization and insolvency of former industrial platforms) presented a unique opportunity for real estate development. These emptied spaces, ripped for (re) development and were in dire need of private capital, offered the potential for significant returns on investment. Additionally, due to their development, these territories increased the exchange value of the surroundings.

Romanian developers dominated residential real estate development, except when the land emptied by deindustrialization was vast (such as Tractorul in Brașov). They invested capital in this business in the capital and regional cities of Romania, being backed up or not by institutional investors.

The capital and regional cities attracted foreign capital for commercial real estate development (retail, including shopping malls and offices). The most significant transactions were made in the office buildings sector, e.g., by NEPI, Globalworth, and AFI Europe.

The Romanian third-tier cities, with their promising potential for investments in retail real estate development (mostly hyper- and supermarkets but also shopping malls), have attracted foreign capital interested in enlarging their global portfolios. For example, Prime Kapital and Atterbury Europe through the Romanian Iulius Group. The population’s eagerness to consume following Western models further enhanced the appeal of these cities for real estate development.

The major food-retail companies also acted as real estate developers (e.g., Lidl, Kaufland, Profi, Auchan, Mega Image, Carrefour, Cora, Metro, and Selgros) wherever they decided to expand, attracting further investments in other real estate sectors.

Being the most profitable, the built-to-rent estates are the most wanted investments by institutional investors or investment funds. Therefore, the latter are active in those segments of real estate markets where built-to-rent is dominant. Earlier, this was the commercial real estate. However, recently, due to the interest rate increase, the residential market is expected to be strongly marked by a turn from homeownership to private rental, indicating a shift in investment opportunities.

After 2014, more multinational retail companies transformed their businesses into mixed-use real estate development and management. They also entered a new phase of financialization, a transition from reliance on bank loans to attracting capital from investment funds. Examples from the REDURB project are Ceetrus and AFI Europe.

The role of deindustrialization in the emergence and advancement of real estate development

Deindustrialization-cum-privatization facilitated the primitive accumulation of capital as it transposed the ownership over the means of production to the hands of the emerging property-owner class. The private property funds created by the state in 1992, responsible for the privatization of factories, owned shares in these enterprises that they could capitalize on later when they were transformed into private equity funds, some with real estate investments. The winners of deindustrialization could direct their capital towards real estate development and investments into funds with shares in real estate. Deindustrialization contributed to the creation of debtors/ entrepreneurs involved in privatization and real estate development, which impacted the flourishing of the banking sector.

Deindustrialization enabled the owners of privatized and bankrupted factories to extract long-term income from renting the lands and buildings usually purchased at a low price from the state to different enterprises, from small productive units through artists to warehouses and sports halls. Deindustrialization emptied spaces on which, when the capital was ready, it could be invested for new residential, retail, or office buildings or mixed-use complexes, from which the owners could combine profit from selling with profit from renting. Lands emptied from industrial production could be used as collateral and catalyst for loans based on land value.

Deindustrialization facilitated the collaboration between local and global capital. It also contributed to the contraction of the productive economy, which benefited consumption-based and financialized growth (as suggested metaphorically by Figure 4, using pictures made in the Redurb research project).

Figure 4. The metamorphosis from production to consumption, from industry to real estate, or from communism to capitalism

What can we learn from real estate development studies in semiperipheries?

Existing real estate literature in urban studies, sociology, and critical geography is mainly about the financialization of real estate development; however, it is based on recognizing the centrality of real estate development in the political economy regime. The REDURB research project revealed the relations between local geographies, global moment, and great transformations, asking how the dismantling of the socialist economy, financial system, and housing regime created a high demand for private capital and opportunities for foreign capital in all of these sectors. Furthermore, REDURB showed that uneven development manifests in uneven real estate development and its uneven financialization across and within countries, as well as peripheralization and unevenness, which advance at different scales. It exhibited that capitalist transformations in Romania (and in CEE) were backed up by a process in which international organizations urged governments to ensure the conditions for the formation of a market economy and catch up with Western development patterns; therefore, REDURB stressed the role of politics, state, and trans-statal actors in economic restructuring.

Existing literature addresses financialization as a process that transforms real estate assets and landed properties into financial assets and creates new capital investment opportunities due to the penetration of the financial markets into the real estate markets. It shows that several segments of the financial markets are connected to the real estate market: the mortgage market, including mortgage securitization; stock and share markets, where diverse investment funds administer large pools of money. The REDURB research project revealed the role of deindustrialization in the emergence and advancement of real estate development, showing that the latter is both a spatial and financial process and, in this way, it re-territorialized the analysis of financialization. Therefore, it could unveil how de-industrialization can be connected to financialization due to various political and economic path dependencies and the current context of transformations.

Existing literature on the financialization of real estate development stresses that investments in real estate development serve the interests of the investors/developers rather than the actual socio-economic needs of people. It shows that when real estate investors/developers are embedded in global capital flows, their investments gain a strong de-contextualized character because they follow the investment logic inherent in their global portfolios. The REDURB research project, completing the existing few initiatives from CEE studying subordinate and uneven financialization and studies conducted in the Global South, re-contextualized the phenomenon at the juncture of local and global actors and processes in the region but kept as central the idea of subordination of real estate and urban development to the interests of capital.

Toward a potential debate

Thinking about possible connections between the REDURB analysis on real estate development as a product and as a constitutive element of capitalist transformations and the Beyond Inhabitation Lab studies about the struggles against contemporary and historical forms of dispossession, one should consider considering the following question. If real estate development for profit is a central pillar of global capitalism as it is, how can we imagine and practice struggles against exploitation and dispossession happening via a capital accumulation regime into which this business is so embedded? What kind of alliances should housing movements look for in their endeavors among social movements with other causes or among political initiatives at local and international levels looking to transgress capitalism?